私人资本宇宙规模已高达22万亿美元,近日美国银行(Bank of America)研究部的顶级分析师揭开了这类资产的面纱:如果将其视为一个国家,其规模堪称“全球第二大经济体”。随着全球金融格局经历巨变,美国银行研究部最新的主题投资报告显示,私人资本正在重塑公司、投资者和经济体对增长、风险与控制的思考方式,不仅挑战了公开市场的主导地位,也为创新与风险防范开辟了新前沿。

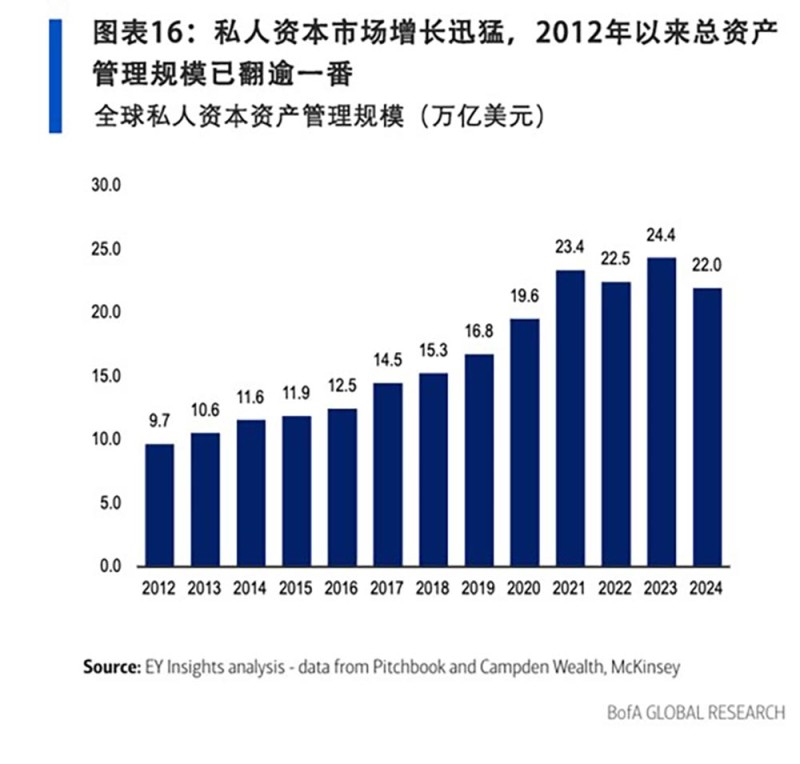

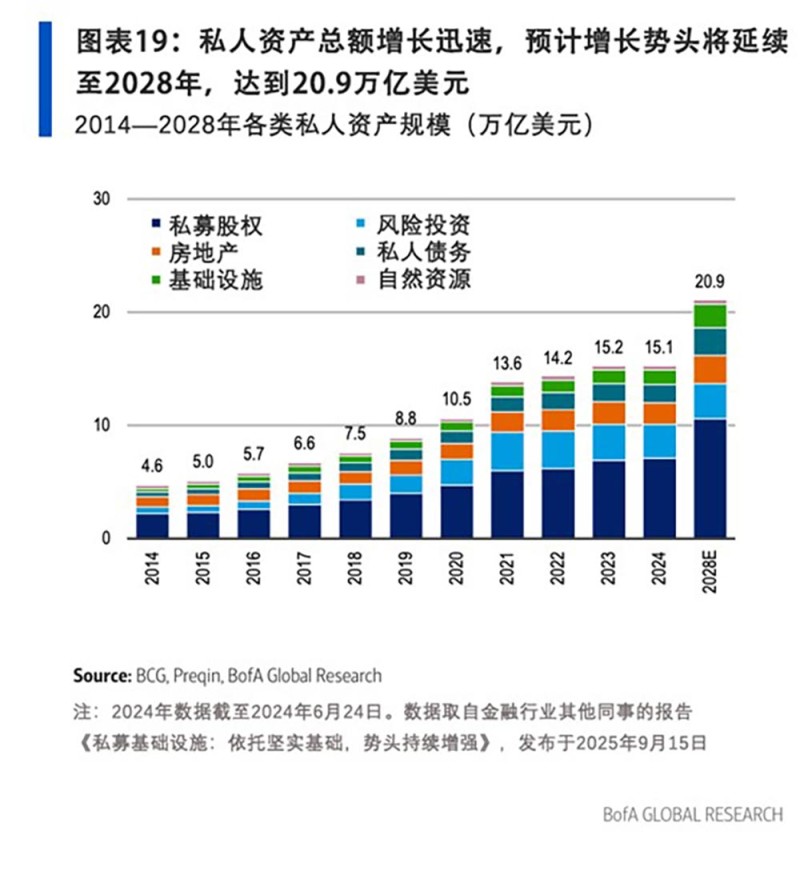

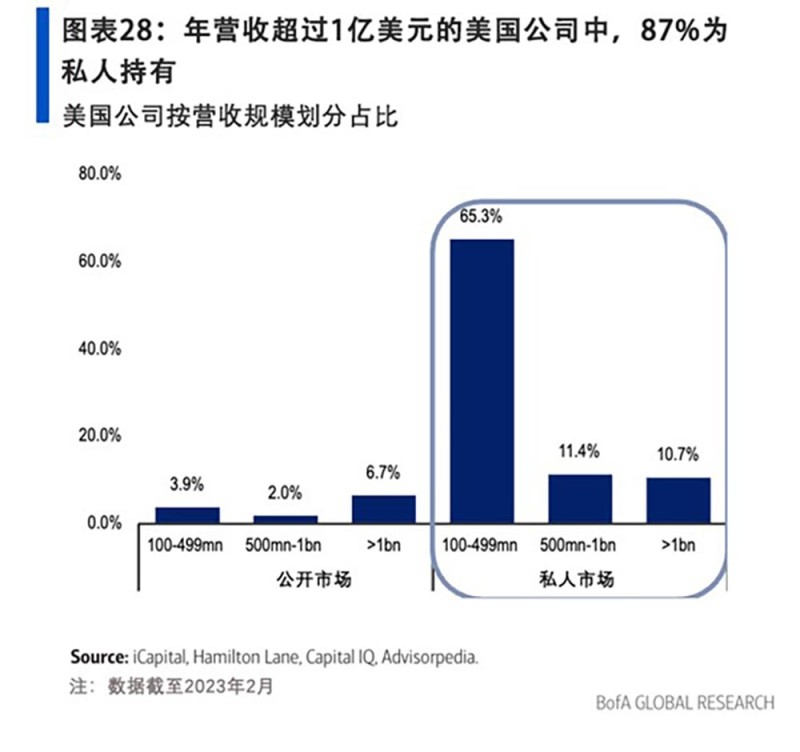

美国银行将私人资本定义为不在公开市场流通的资产,包括私募股权、私人信贷和实物资产等。其增长速度惊人,自2012年以来规模增长超过一倍,到2024年已达22万亿美元。这一爆炸性增长主要源于企业从公开市场撤退的趋势。自2000年以来,美国上市公司数量减半,仅剩4000多家,而获得风险资本支持的私人公司数量却飙升了25倍。如今,初创公司平均保持私有状态长达16年,比十年前延长了三分之一,这反映出企业正广泛转向私人资本,以规避公开市场的审查和监管。

美国银行认为,全球最具变革性的公司并不在股票市场上交易。正如公开股票市场有“七巨头”一样,私人市场也存在由“千亿兽”(估值达到或超过1000亿美元且仍在增长)组成的“私人市场七巨头”。美国银行主题研究团队估计,自2023年以来,这些公司的总估值已飙升近五倍,达到1.4万亿美元。他们评估了该领域顶部的16家公司,其总价值达1.5万亿美元,占全球GDP的1%,这一数字令人震惊。此外,榜单上还有众多“百亿兽”(估值超过100亿美元)和独角兽公司。

美国银行发现,对投资者而言,在此期间私募股权的表现明显优于标准普尔500指数,平均每年高出六个百分点。美国银行分析师补充道,私有化还有其他好处:“每年花在金融监管文书工作上的时间,足以建造12座吉萨大金字塔。”

但随着这类资产规模膨胀,金融专家警告称,不透明性会滋生风险,尤其是规模在1万亿至3万亿美元之间的私人信贷板块。公开市场具备透明度、治理机制和流动性;相比之下,私人公司往往避免定期报告,受到的监管也较为宽松。这种信息不透明可能掩盖财务和治理隐患,分析师因此提醒投资者,在追求回报的同时切勿忽视潜在风险。

过去一个月,次级贷款机构Tricolor Holdings和汽车供应商First Brands因涉嫌欺诈和亏损事件破产,导致美国银行股市值蒸发1000亿美元,华尔街的“恐慌指数”VIX随之飙升超过35%。摩根大通(JPMorgan)首席执行官杰米·戴蒙(Jamie Dimon)指出私人借贷市场暗藏风险,并警告称:“当你发现一只蟑螂时,很可能已经有一群了。”事实上,戴蒙至少从5月起就一直在发出类似警告,当时他表示非银行贷款“尚未经历经济下行期的考验”,暗示一旦经济衰退来临,可能引发一波违约潮。

资本配置转向私人领域

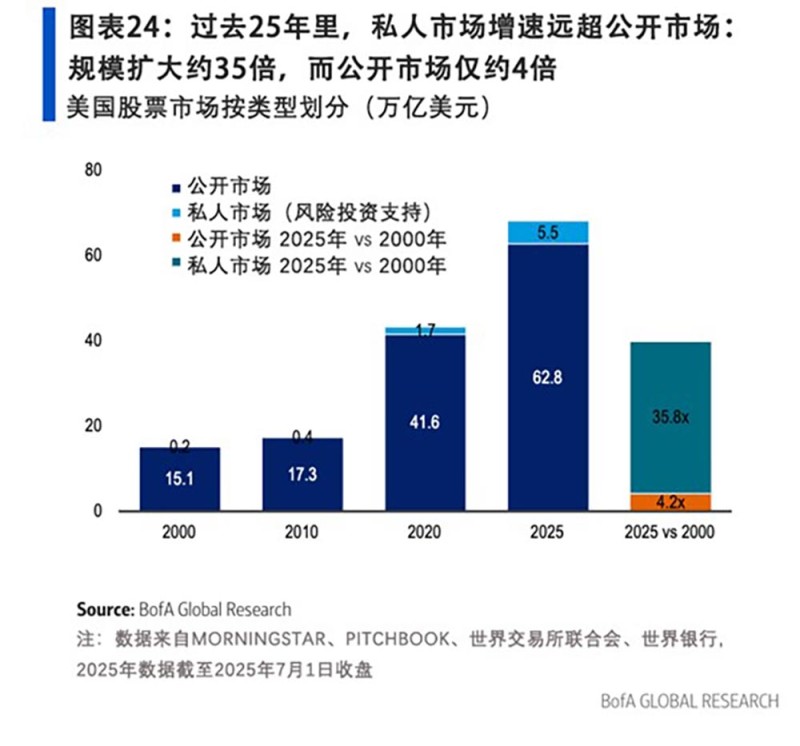

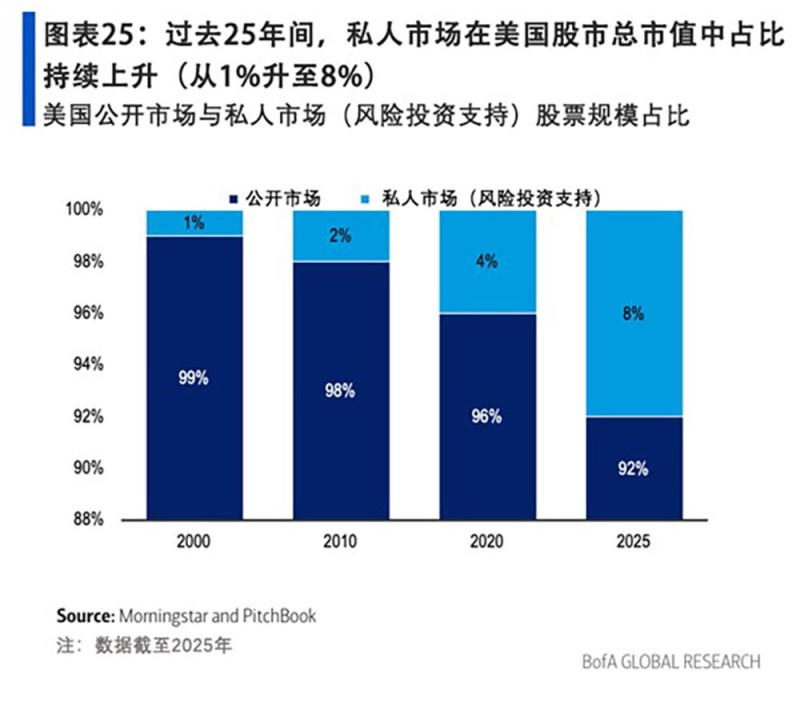

历史上,上市公司曾被视为资本效率的最佳载体。它们提供流动性投资、透明的财务信息,并且对所有投资者开放。然而,私人资本正在改写规则。随着寻求IPO的公司减少,公开市场在经济增长中一度占据的核心地位正逐渐丧失。与此同时,由OpenAI的ChatGPT等颠覆性技术引发的创新和数字化浪潮,正日益得到资金雄厚的私人投资者的支持。美国银行发现,自ChatGPT推出以来,英伟达(Nvidia)、谷歌(Google)、微软(Microsoft)和亚马逊(Amazon)已投资了全球约半数的人工智能独角兽公司。

此外,推动GDP增长重要部分的数据中心交易也越来越依赖于私人信贷。例如,据彭博社报道,Meta(脸书)已为路易斯安那州的一个数据中心敲定了近300亿美元的融资方案,并称这是有记录以来最大的私人资本交易。该领域的支出规模空前,仅OpenAI一家公司就估计需要数万亿美元的基础设施投入,以满足快速发展的技术需求。10月下旬,阿波罗全球管理公司(Apollo Global Management)首席经济学家托斯滕·斯洛克(Torsten Slok)指出,数据中心的私人建设支出极为庞大,导致“目前除了AI领域,企业资本支出基本没有增长”。

即便是这一趋势的受益者中也有人表示担忧。OpenAI的首席执行官萨姆·奥特曼(Sam Altman)将其与互联网泡沫相提并论,并警告说“有人会蒙受损失”——尤其根据麻省理工学院一项被广泛引用的研究,据报道95%的生成式AI项目未能产生任何利润。分析师警告称,如果投机性基础设施投资超过了实际效用或收入,投资者可能遭受损失,这让人回想起21世纪初电信业过度扩张的教训。

AI建设的第一阶段主要是点对点融资,但现在债券投资者和私人信贷贷款方提供的资金是公开市场的两到三倍。科技“超大规模企业”已利用私人信贷获得了期限较长的可持续贷款,摩根大通当时估计,8月份与AI基础设施相关的商业抵押贷款支持证券规模达到156亿美元。如今的大型交易融资期限多为20至30年——这是对技术下的非凡赌注,而这些技术在五年后的商业可行性仍不确定。标普全球评级(S&P Global Ratings)私人市场分析全球主管鲁斯·杨(Ruth Yang)在8月告诉彭博社:“我们对未来现金流的评估比较保守,因为我们不知道它们会是什么样子,没有历史依据可供参考。”

长期为《财富》报道私人信贷领域的肖恩·图利(Shawn Tully)指出,阿波罗(Apollo)、阿瑞斯(Ares)和KKR等主要参与者与其他机构有所不同,它们正“开创一种高度原创的策略,独立发放信贷,通常由从铁路车辆到数据中心等高收益资产支持,并能锁定借款人多年。”借款人愿意支付比传统银团贷款高得多的利息,以避免漫长、昂贵且需要标普和惠誉评级、严格契约条款有时耗时良久的银团贷款流程。

该领域的两位顶级高管——Runway Growth Capital的大卫·斯普伦(David Spreng)和BC Partners Credit的泰德·戈德索普(Ted Goldthorpe)在本月《财富》的一篇评论文章中认为,私人信贷实际上并非神秘的怪物,而是“建立在现金流、企业价值和下行保护基础上的结构化融资。”他们指出,这与风险投资式的冒险相去甚远,许多私人债务工具是公开上市或有机构支持的,同时报告经审计的财务报表,并在法律和信托义务下运作。他们补充说,诚然,市场中存在标准较宽松的风险较高部分,例如低约束贷款、激进的结构化设计或在底层资产缺乏流动性时承诺提供流动性。

本月早些时候,摩根士丹利(Morgan Stanley)财富管理首席投资官丽莎·沙利特(Lisa Shalett)告诉《财富》,她特别担忧当前的支出热潮在多大程度上是由私人信贷驱动的。“每天早晨我打开彭博终端,第一眼看到的就是甲骨文(Oracle)债务的信用违约互换利差情况,”她提到的是信用违约互换,这种金融工具在2008年全球金融危机市场崩溃中扮演的角色使其臭名昭著。“如果人们开始担心甲骨文的偿付能力,”沙利特说,“那对我们来说将是一个早期迹象,表明市场开始紧张了。”

长远视角:机遇与监管的平衡

向私人投资的结构性转变对社会具有深远影响。美国银行分析师指出,随着私人公司规模扩大,它们正在影响技术发展方式、就业创造模式以及风险管理方法。目前排名前120的私人独角兽总估值约等于德国股市总市值,这表明它们在全球舞台上拥有巨大的影响力。

巴克莱(Barclays)股东咨询集团全球负责人吉姆·罗斯曼(Jim Rossman)在华尔街追踪私人资产已数十年,尤其关注对冲基金,他看到了更广泛的变革正在发生。“私人资本的增长确实反映了一个事实:公司,特别是像阿波罗、黑石(Blackstone)和TPG这样的公司,正接近万亿美元的平台规模,”他在最近接受《财富》采访时表示,并指出在某些情况下,这些公司已经收购了自己的保险公司,其发展已超越了传统投资公司的概念。

罗斯曼说,这些公司拥有充裕的资本和资产,他认为私人资本的繁荣正在催生公开市场之外的替代平台的发展。“你可能会看到一个时代,私募股权、私人资本让公司能够以私有形式存在更长时间。如果401(k)计划向私募股权投资开放,”他补充道,他可以设想某种投资平台,财富顾问可以像现在投资股票一样自由地投资私人资本领域。“那将使你接触到比公开市场更广泛的经济领域。”

罗斯曼进一步表示,总的来说,金融世界正在经历许多变化。“我认为存在技术变革、代际变革,而最终可能最重要的结构性变革是共同基金投资的增长。”罗斯曼认为,不应将私人资本视为神秘且高风险的事物,它实际上正在向投资开放更多类型的公司,这一趋势可能会持续发展,甚至以许多投资者意想不到的方式演变。

罗斯曼回忆起在20世纪90年代末通过一家领先的资产管理公司购买他的第一只共同基金:“加入成本是300个基点,即三个百分点,他们会挑选28家有潜力的科技公司……然后,哦,年费率还要2.5%,即250个基点。”他说,如今,指数基金革命已经普及了投资渠道,你只需5、15或25个基点就能买到同样的基金。“这简直不可思议。”

随着公共资本与私人资本之间的界限变得模糊,这个22万亿美元的私人资本世界不仅仅是一个金融故事——它更是一个路标,预示着未来我们的经济、公司和创新将如何构建和估值。私人资产的规模已可与国家经济体量相媲美,科技巨头们在公众视野之外进行巨额押注,顶尖分析师认为,这场革命才刚刚开始。(*)

译者:梁宇

审校:夏林

私人资本宇宙规模已高达22万亿美元,近日美国银行(Bank of America)研究部的顶级分析师揭开了这类资产的面纱:如果将其视为一个国家,其规模堪称“全球第二大经济体”。随着全球金融格局经历巨变,美国银行研究部最新的主题投资报告显示,私人资本正在重塑公司、投资者和经济体对增长、风险与控制的思考方式,不仅挑战了公开市场的主导地位,也为创新与风险防范开辟了新前沿。

美国银行将私人资本定义为不在公开市场流通的资产,包括私募股权、私人信贷和实物资产等。其增长速度惊人,自2012年以来规模增长超过一倍,到2024年已达22万亿美元。这一爆炸性增长主要源于企业从公开市场撤退的趋势。自2000年以来,美国上市公司数量减半,仅剩4000多家,而获得风险资本支持的私人公司数量却飙升了25倍。如今,初创公司平均保持私有状态长达16年,比十年前延长了三分之一,这反映出企业正广泛转向私人资本,以规避公开市场的审查和监管。

美国银行认为,全球最具变革性的公司并不在股票市场上交易。正如公开股票市场有“七巨头”一样,私人市场也存在由“千亿兽”(估值达到或超过1000亿美元且仍在增长)组成的“私人市场七巨头”。美国银行主题研究团队估计,自2023年以来,这些公司的总估值已飙升近五倍,达到1.4万亿美元。他们评估了该领域顶部的16家公司,其总价值达1.5万亿美元,占全球GDP的1%,这一数字令人震惊。此外,榜单上还有众多“百亿兽”(估值超过100亿美元)和独角兽公司。

美国银行发现,对投资者而言,在此期间私募股权的表现明显优于标准普尔500指数,平均每年高出六个百分点。美国银行分析师补充道,私有化还有其他好处:“每年花在金融监管文书工作上的时间,足以建造12座吉萨大金字塔。”

但随着这类资产规模膨胀,金融专家警告称,不透明性会滋生风险,尤其是规模在1万亿至3万亿美元之间的私人信贷板块。公开市场具备透明度、治理机制和流动性;相比之下,私人公司往往避免定期报告,受到的监管也较为宽松。这种信息不透明可能掩盖财务和治理隐患,分析师因此提醒投资者,在追求回报的同时切勿忽视潜在风险。

过去一个月,次级贷款机构Tricolor Holdings和汽车供应商First Brands因涉嫌欺诈和亏损事件破产,导致美国银行股市值蒸发1000亿美元,华尔街的“恐慌指数”VIX随之飙升超过35%。摩根大通(JPMorgan)首席执行官杰米·戴蒙(Jamie Dimon)指出私人借贷市场暗藏风险,并警告称:“当你发现一只蟑螂时,很可能已经有一群了。”事实上,戴蒙至少从5月起就一直在发出类似警告,当时他表示非银行贷款“尚未经历经济下行期的考验”,暗示一旦经济衰退来临,可能引发一波违约潮。

资本配置转向私人领域

历史上,上市公司曾被视为资本效率的最佳载体。它们提供流动性投资、透明的财务信息,并且对所有投资者开放。然而,私人资本正在改写规则。随着寻求IPO的公司减少,公开市场在经济增长中一度占据的核心地位正逐渐丧失。与此同时,由OpenAI的ChatGPT等颠覆性技术引发的创新和数字化浪潮,正日益得到资金雄厚的私人投资者的支持。美国银行发现,自ChatGPT推出以来,英伟达(Nvidia)、谷歌(Google)、微软(Microsoft)和亚马逊(Amazon)已投资了全球约半数的人工智能独角兽公司。

此外,推动GDP增长重要部分的数据中心交易也越来越依赖于私人信贷。例如,据彭博社报道,Meta(脸书)已为路易斯安那州的一个数据中心敲定了近300亿美元的融资方案,并称这是有记录以来最大的私人资本交易。该领域的支出规模空前,仅OpenAI一家公司就估计需要数万亿美元的基础设施投入,以满足快速发展的技术需求。10月下旬,阿波罗全球管理公司(Apollo Global Management)首席经济学家托斯滕·斯洛克(Torsten Slok)指出,数据中心的私人建设支出极为庞大,导致“目前除了AI领域,企业资本支出基本没有增长”。

即便是这一趋势的受益者中也有人表示担忧。OpenAI的首席执行官萨姆·奥特曼(Sam Altman)将其与互联网泡沫相提并论,并警告说“有人会蒙受损失”——尤其根据麻省理工学院一项被广泛引用的研究,据报道95%的生成式AI项目未能产生任何利润。分析师警告称,如果投机性基础设施投资超过了实际效用或收入,投资者可能遭受损失,这让人回想起21世纪初电信业过度扩张的教训。

AI建设的第一阶段主要是点对点融资,但现在债券投资者和私人信贷贷款方提供的资金是公开市场的两到三倍。科技“超大规模企业”已利用私人信贷获得了期限较长的可持续贷款,摩根大通当时估计,8月份与AI基础设施相关的商业抵押贷款支持证券规模达到156亿美元。如今的大型交易融资期限多为20至30年——这是对技术下的非凡赌注,而这些技术在五年后的商业可行性仍不确定。标普全球评级(S&P Global Ratings)私人市场分析全球主管鲁斯·杨(Ruth Yang)在8月告诉彭博社:“我们对未来现金流的评估比较保守,因为我们不知道它们会是什么样子,没有历史依据可供参考。”

长期为《财富》报道私人信贷领域的肖恩·图利(Shawn Tully)指出,阿波罗(Apollo)、阿瑞斯(Ares)和KKR等主要参与者与其他机构有所不同,它们正“开创一种高度原创的策略,独立发放信贷,通常由从铁路车辆到数据中心等高收益资产支持,并能锁定借款人多年。”借款人愿意支付比传统银团贷款高得多的利息,以避免漫长、昂贵且需要标普和惠誉评级、严格契约条款有时耗时良久的银团贷款流程。

该领域的两位顶级高管——Runway Growth Capital的大卫·斯普伦(David Spreng)和BC Partners Credit的泰德·戈德索普(Ted Goldthorpe)在本月《财富》的一篇评论文章中认为,私人信贷实际上并非神秘的怪物,而是“建立在现金流、企业价值和下行保护基础上的结构化融资。”他们指出,这与风险投资式的冒险相去甚远,许多私人债务工具是公开上市或有机构支持的,同时报告经审计的财务报表,并在法律和信托义务下运作。他们补充说,诚然,市场中存在标准较宽松的风险较高部分,例如低约束贷款、激进的结构化设计或在底层资产缺乏流动性时承诺提供流动性。

本月早些时候,摩根士丹利(Morgan Stanley)财富管理首席投资官丽莎·沙利特(Lisa Shalett)告诉《财富》,她特别担忧当前的支出热潮在多大程度上是由私人信贷驱动的。“每天早晨我打开彭博终端,第一眼看到的就是甲骨文(Oracle)债务的信用违约互换利差情况,”她提到的是信用违约互换,这种金融工具在2008年全球金融危机市场崩溃中扮演的角色使其臭名昭著。“如果人们开始担心甲骨文的偿付能力,”沙利特说,“那对我们来说将是一个早期迹象,表明市场开始紧张了。”

长远视角:机遇与监管的平衡

向私人投资的结构性转变对社会具有深远影响。美国银行分析师指出,随着私人公司规模扩大,它们正在影响技术发展方式、就业创造模式以及风险管理方法。目前排名前120的私人独角兽总估值约等于德国股市总市值,这表明它们在全球舞台上拥有巨大的影响力。

巴克莱(Barclays)股东咨询集团全球负责人吉姆·罗斯曼(Jim Rossman)在华尔街追踪私人资产已数十年,尤其关注对冲基金,他看到了更广泛的变革正在发生。“私人资本的增长确实反映了一个事实:公司,特别是像阿波罗、黑石(Blackstone)和TPG这样的公司,正接近万亿美元的平台规模,”他在最近接受《财富》采访时表示,并指出在某些情况下,这些公司已经收购了自己的保险公司,其发展已超越了传统投资公司的概念。

罗斯曼说,这些公司拥有充裕的资本和资产,他认为私人资本的繁荣正在催生公开市场之外的替代平台的发展。“你可能会看到一个时代,私募股权、私人资本让公司能够以私有形式存在更长时间。如果401(k)计划向私募股权投资开放,”他补充道,他可以设想某种投资平台,财富顾问可以像现在投资股票一样自由地投资私人资本领域。“那将使你接触到比公开市场更广泛的经济领域。”

罗斯曼进一步表示,总的来说,金融世界正在经历许多变化。“我认为存在技术变革、代际变革,而最终可能最重要的结构性变革是共同基金投资的增长。”罗斯曼认为,不应将私人资本视为神秘且高风险的事物,它实际上正在向投资开放更多类型的公司,这一趋势可能会持续发展,甚至以许多投资者意想不到的方式演变。

罗斯曼回忆起在20世纪90年代末通过一家领先的资产管理公司购买他的第一只共同基金:“加入成本是300个基点,即三个百分点,他们会挑选28家有潜力的科技公司……然后,哦,年费率还要2.5%,即250个基点。”他说,如今,指数基金革命已经普及了投资渠道,你只需5、15或25个基点就能买到同样的基金。“这简直不可思议。”

随着公共资本与私人资本之间的界限变得模糊,这个22万亿美元的私人资本世界不仅仅是一个金融故事——它更是一个路标,预示着未来我们的经济、公司和创新将如何构建和估值。私人资产的规模已可与国家经济体量相媲美,科技巨头们在公众视野之外进行巨额押注,顶尖分析师认为,这场革命才刚刚开始。(*)

译者:梁宇

审校:夏林

Top analysts at Bank of America Research are pulling back the curtain on the colossal $22 trillion universe of private capital, an asset class so massive it would be “the world's second-largest economy” if it were treated as a country. As the global financial landscape faces tectonic shifts, Bank of America Research's latest thematic investing report reveals that private capital is reshaping how companies, investors, and economies think about growth, risk, and control, challenging the primacy of public markets and opening new frontiers for both innovation and caution.

Private capital, defined by the bank as assets not available on public markets, includes private equity, private credit and real assets. It has multiplied at a staggering pace, more than doubling since 2012 to $22 trillion by 2024. This explosion has been driven by a retreat from public markets. Since 2000, the number of U.S.-listed companies has halved to just over 4,000, even as the number of private venture-backed firms soared 25-fold. Startups now remain private for an average of 16 years, a third longer than a decade ago, reflecting a broad shift toward private capital and away from public scrutiny and regulation.

The world's most transformative firms aren't found on the stock market ticker, BofA argues. Just as public stock markets have a “Magnificent 7,” so there is a “Private Magnificent 7” of “hectocorns,” each valued at $100 billion or more and growing. BofA's Thematic Research team estimates that their combined valuations have skyrocketed nearly fivefold since 2023 to $1.4 trillion. They evaluated the top 16 companies in the space, representing $1.5 trillion in value, an astonishing 1% of global GDP. There are many other “decacorns” (valued at $10 billion+) and unicorns below them in the list.

For investors, BofA finds that private equity has notably outperformed the S&P 500 over this period, by six percentage points per year on average. And there are other benefits to privacy, BofA analysts add: “In the time spent on financial regulation paperwork every year, 12 Great Pyramids of Giza could be built.”

But as this asset class balloons, financial experts warn that opacity breeds risk, especially with regard to the $1 trillion-$3 trillion chunk of the asset class known as private credit. Public markets offer transparency, governance, and liquidity; private firms, by contrast, often avoid periodic reporting and undergo less rigorous oversight. This lack of visibility can mask financial and governance hazards, with analysts urging investors not to overlook the pitfalls in their quest for returns.

Wall Street's “fear index”---the VIX---spiked by more than 35% in the past month amid bankruptcies at subprime lender Tricolor Holdings and auto supplier First Brands, both marred by alleged fraud and loss events, slicing $100 billion off U.S. bank stock market capitalization. JPMorgan CEO Jamie Dimon warned, “When you see one cockroach, there are probably more,” pointing to the dangers of hidden risks in private lending markets. In fact, Dimon has been sounding a similar tune since at least May, when he warned that non-bank lending ”hasn't been tested in a downturn,” implying that a deluge of defaults could follow if a recession hits.

Capital allocation goes private

Historically, public companies were seen as the best vehicles for capital efficiency. They offered liquid investments, transparent financials, and were accessible to all. Yet, private capital is rewriting the rules. With fewer companies pursuing IPOs, public markets are losing their once-central role in economic growth. At the same time, innovation and digitization---sparked by disruptors like OpenAI's ChatGPT---are increasingly nourished by deep-pocketed private investors. Since ChatGPT's launch, BofA finds, Nvidia, Google, Microsoft, and Amazon have invested in roughly half of the world's 100 artificial intelligence (AI) unicorns.

The data-center deals that are driving a significant chunk of GDP growth are increasingly based on private credit, to boot. Meta, for example, has secured a nearly $30 billion financing package or a data center in Louisiana, Bloomberg reported, adding that it is the largest private capital deal on record. The scale of spending in this space is unprecedented, with OpenAI alone estimating it will require trillions in infrastructure spend to keep up with rapid technological demands. In late October, Apollo Global Management Chief Economist Torsten Slok argued that private construction spending on data centers was so massive that there was “basically no growth in corporate capex outside of AI at this moment.”

Even some of the beneficiaries of this are concerned. OpenAI's CEO Sam Altman has drawn parallels to the dot-com bubble, cautioning that “someone's gonna get burned there”---especially since 95% of generative AI projects reportedly don't deliver any profit, according to a widely read piece of MIT research. Analysts warn that investors could face pain if speculative infrastructure bets outpace real-world utility or revenues, recalling lessons from early-2000s telecom overreach.

The first phase of AI build-out was largely peer-to-peer, but now bond investors and private credit lenders are providing two to three times the funding of public markets. Tech “hyperscalers” have tapped private credit for sustained, long-tenor loans, and commercial mortgage-backed securities tied to AI infrastructure hit $15.6 billion in August, JPMorgan estimated at the time. Major deals now feature 20-30 year funding horizons---extraordinary bets on technologies whose commercial viability five years from now remains uncertain. “We are conservative in our assessment of forward cash flows because we don't know what they will look like, there's no historical basis,” Ruth Yang, global head of private market analytics at S&P Global Ratings, told Bloomberg in August.

Shawn Tully, who has reported extensively on private credit for Fortune, noted a distinction between major players such as Apollo, Ares, and KKR, who are “pioneering a highly original strategy by extending credit they originate independently, often backed by high-earning assets from rail cars to data centers, that lock in borrowers for a number of years.” Borrowers are willing to pay a lot more in interest than the traditional lengthy, expensive syndication process that requires ratings from S&P and Fitch, tough covenants, and sometimes long.

Two top executives in the space, David Spreng of Runway Growth Capital and Ted Goldthorpe of BC Partners Credit, argued in a Fortune commentary this month that private credit is not, in fact, a shadowy bogeyman but “structured finance built on cash flow, enterprise value, and downside protection.” Far from venture-style risk-taking, they argue that many private debt vehicles are publicly listed or institutionally backed, while reporting audited financials and operating under legal and fiduciary obligations. To be sure, they add, there are riskier parts of the market with looser standards such as covenant-lite loans, aggressive structures, or promises of liquidity where underlying assets are illiquid.

Earlier this month, Morgan Stanley Wealth Management CIO Lisa Shalett told Fortune she was particularly concerned about how much of the spending boom has been driven by private credit. “Every morning the opening screen on my Bloomberg is what's going on with CDS spreads on Oracle debt,” she said, referring to credit default swaps, the financial instrument infamous for the role it played in the 2008 Great Financial Crisis global market meltdown. “If people start getting worried about Oracle's ability to pay,” Shalett said, “that's gonna be an early indication to us that people are getting nervous.”

The long view: opportunity vs. Oversight

The tectonic shift toward private investing carries enormous implications for society. BofA analysts note that as private firms scale, they shape how technology develops, how jobs are created, and how risks are managed. The top 120 private unicorns now boast a total valuation roughly equal to Germany's entire market cap, signaling their outsized influence on the global stage.

Jim Rossman, the global head of Barclays' shareholder advisory group, has been tracking private assets with a particular focus on hedge funds for decades on Wall Street, and he sees a wider transformation taking place. “The growth of private capital is really a reflection of the fact that companies, particularly these now that Apollo and Blackstone and TPG, are closing in on trillion-dollar platforms,” he told Fortune in a recent interview, noting that they've acquired their own insurance companies in some cases and are growing beyond the traditional conception of an investment firm.

These firms are so flush with capital and assets, Rossman said, that he sees the private capital boom facilitating the growth of alternative platforms to public markets. “You could see an age when private equity, private capital allows companies to remain in a private format for longer. And if 401(k)s get opened up” for private equity investments, he added, he could envision some kind of investment platform where wealth advisors could invest money just as freely in the private capital space as they can now in equities. “And that would give you exposure to a much broader part of the economy than just what's public.”

More generally, Rossman added, the world of finance is undergoing many changes. “I think there's a technology change, a generational change, and then finally, the structural change [that] may be the most important is the growth of mutual fund investing.” Instead of seeing private capital as a shadowy and risky thing, Rossman argued it is opening up more kinds of companies to investment, and that will likely grow, even mutate in surprising ways to many investors.

Rossman recalled buying his first mutual fund through a leading asset manager in the late 1990s: “It cost 300 basis points, three percentage points to join, and they would select 28 interesting technology companies ... and then, oh, the expense ratio would be two-and-a-half, 250 basis points a year.” Today, he said, the index-fund revolution has democratized access to the point where you can get the same fund for just 5, 15 or 25 basis points. “It's just so incredible.”

As the line between public and private capital blurs, the $22 trillion world of private capital is not just a financial story---it's a signpost for how our economies, companies, and innovations will be built and valued in the years to come. With private assets rivaling the size of national economies and the biggest names in tech betting big outside the public eye, top analysts believe this is a revolution that's just getting started.