• 分析人士警告称,少数科技巨头(尤其是英伟达)估值过高,已在美股中形成类似历史泡沫时期的集中度风险。

标普500指数周三下跌0.69%。英伟达(Nvidia)跌幅超过两倍,下跌1.95%。此外,由于投资者对依赖融资的政府信誉丧失信心,债市对长期收益率走高反应消极。

整体市场情绪略显紧张。

德意志银行近日发布的一份研究报告更是火上浇油,直指核心问题:“美国股市是否正处在泡沫之中?”根据分析师吉姆·里德(Jim Reid)、亨利·艾伦(Henry Allen)和拉杰谢卡尔·巴塔查里亚(Rajsekhar Bhattacharyya)的观点,答案或许是肯定的。

他们指出,英伟达是造成泡沫风险问题的重要驱动因素。它的市值非常庞大。是不是过于庞大了?

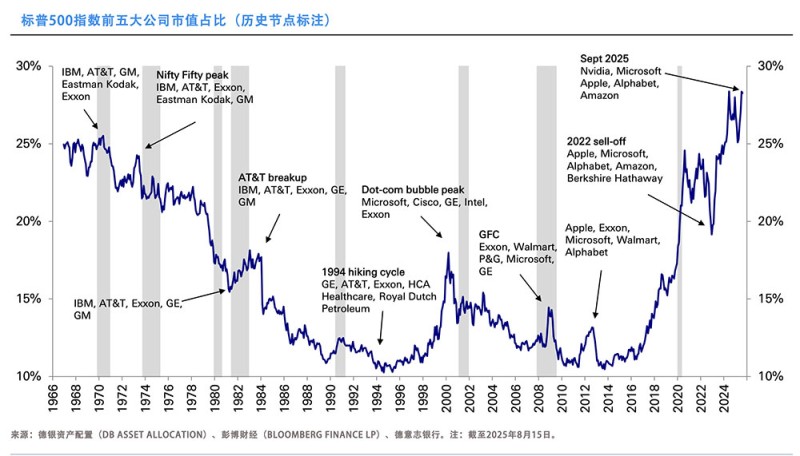

三位分析师在报告中写道:“英伟达的市值,如今已经超过除美国、中国、日本和印度之外世界上任何一个国家的整个股票市场的总市值。”这种现象扭曲了美国股市格局,因为英伟达与另外四家公司(微软、Alphabet、苹果和亚马逊)合计占据标普500指数总市值的30%。相比之下,在2000年互联网泡沫时期,标普500前五大公司的集中度还不到这个数字的一半。

下图清晰展示了当前市场对前五大股票的高度依赖程度:

这些股票的估值之高,已使美国股市规模以史无前例的方式远超海外市场。报告指出:“美国股市现在的规模几乎是排名第二的中国的五倍,约为欧洲主要市场的20倍。”

德意志银行团队表示:“这并不意味着一定存在泡沫,但我们似乎正处在未知领域,且市场表现很可能高度依赖少数几家公司。”

“值得注意的是,在发达国家股市中,唯有美国可能存在泡沫风险。其他七国集团(G7)当前股市估值与盈利相比仍处于历史平均水平。”

那还能出什么问题呢?

劳动力市场就是一个隐患。

安永-帕特农(EY-Parthenon)首席经济学家格雷戈里·达科(Gregory Daco)在一份报告中写道:“8月就业报告很可能证实劳动力市场正在明显放缓,原因是,企业领导者正面临终端需求减弱、成本与利率上升以及不确定性加剧等多重挑战,因此持续收紧招聘。”

“我们预计就业增长将进一步放缓,8月非农就业人数增幅仅为4万,低于7月的7.3万增幅。失业率预计将小幅上升至4.3%,创2021年10月以来新高。”

请系好安全带,前方将颠簸难行。换句话说,衡量市场波动性的VIX恐慌指数近日持续走高,昨日上涨5.46%。(*)

译者:刘进龙

审校:汪皓

• 分析人士警告称,少数科技巨头(尤其是英伟达)估值过高,已在美股中形成类似历史泡沫时期的集中度风险。

标普500指数周三下跌0.69%。英伟达(Nvidia)跌幅超过两倍,下跌1.95%。此外,由于投资者对依赖融资的政府信誉丧失信心,债市对长期收益率走高反应消极。

整体市场情绪略显紧张。

德意志银行近日发布的一份研究报告更是火上浇油,直指核心问题:“美国股市是否正处在泡沫之中?”根据分析师吉姆·里德(Jim Reid)、亨利·艾伦(Henry Allen)和拉杰谢卡尔·巴塔查里亚(Rajsekhar Bhattacharyya)的观点,答案或许是肯定的。

他们指出,英伟达是造成泡沫风险问题的重要驱动因素。它的市值非常庞大。是不是过于庞大了?

三位分析师在报告中写道:“英伟达的市值,如今已经超过除美国、中国、日本和印度之外世界上任何一个国家的整个股票市场的总市值。”这种现象扭曲了美国股市格局,因为英伟达与另外四家公司(微软、Alphabet、苹果和亚马逊)合计占据标普500指数总市值的30%。相比之下,在2000年互联网泡沫时期,标普500前五大公司的集中度还不到这个数字的一半。

下图清晰展示了当前市场对前五大股票的高度依赖程度:

这些股票的估值之高,已使美国股市规模以史无前例的方式远超海外市场。报告指出:“美国股市现在的规模几乎是排名第二的中国的五倍,约为欧洲主要市场的20倍。”

德意志银行团队表示:“这并不意味着一定存在泡沫,但我们似乎正处在未知领域,且市场表现很可能高度依赖少数几家公司。”

“值得注意的是,在发达国家股市中,唯有美国可能存在泡沫风险。其他七国集团(G7)当前股市估值与盈利相比仍处于历史平均水平。”

那还能出什么问题呢?

劳动力市场就是一个隐患。

安永-帕特农(EY-Parthenon)首席经济学家格雷戈里·达科(Gregory Daco)在一份报告中写道:“8月就业报告很可能证实劳动力市场正在明显放缓,原因是,企业领导者正面临终端需求减弱、成本与利率上升以及不确定性加剧等多重挑战,因此持续收紧招聘。”

“我们预计就业增长将进一步放缓,8月非农就业人数增幅仅为4万,低于7月的7.3万增幅。失业率预计将小幅上升至4.3%,创2021年10月以来新高。”

请系好安全带,前方将颠簸难行。换句话说,衡量市场波动性的VIX恐慌指数近日持续走高,昨日上涨5.46%。(*)

译者:刘进龙

审校:汪皓

• U.S. stocks slid as the S&P 500 fell 0.69% and Nvidia dropped 1.95% yesterday. Analysts warn that outsize valuations in a few tech giants (especially Nvidia) have created a concentration risk in U.S. stocks reminiscent of past bubbles.

The S&P 500 lost 0.69% yesterday. Nvidia, however, lost more than twice that—down 1.95%. Additionally, the bond market is unhappy with long-term yields going up as investors lose faith in the credibility of governments who want their financing.

It’s all looking a bit nervy.

That won’t be helped by a research note from Deutsche Bank today, which asks the question, “Are U.S. equities in a bubble?” The answer, according to analysts Jim Reid, Henry Allen, and Rajsekhar Bhattacharyya, is maybe.

Nvidia is a big part of the problem, they say. Its market cap is huge. Too huge?

“Nvidia’s market cap is now larger than every country’s entire listed stock exchange apart from the U.S., China, Japan, and India,” the trio wrote. That has a distorting effect on U.S. stocks because Nvidia and just four other stocks (Microsoft, Alphabet, Apple, and Amazon) compose 30% of the S&P 500’s entire value. For comparison, the concentration of the top five companies in the S&P during the dotcom bubble of 2000 was less than half that.

This chart shows just how weighted toward the top five stocks the market currently is:

The valuation of those stocks is so high that the U.S. market now dwarfs foreign markets in a way that it historically did not. “The U.S. is now nearly five times larger than China (in second) and around 20 times larger than Europe’s larger markets,” they said.

“This doesn’t automatically mean it’s a bubble, but we appear to be in uncharted territory, and likely means performance heavily depends on a handful of companies,” the Deutsche team said.

“We should note that, of [developed country] equity markets, only the U.S. could be considered a bubble risk. Other G7 equity markets currently have historically average valuations vs. earnings.”

What could possibly go wrong?

The labor market for one thing. The U.S. will publish a new job openings report today (the so-called JOLTS) and a new nonfarm payrolls number on Friday.

EY-Parthenon chief economist Gregory Daco forecasted in a note yesterday that he expects Friday’s employment number to be weak: “August’s employment report is likely to confirm that a marked slowdown in labor market conditions is underway, as business leaders—grappling with softer final demand, higher costs and interest rates, and elevated uncertainty—continue to restrain hiring.

“We anticipate another step down in job growth, with nonfarm payrolls expected to rise by just 40,000 in August, following a 73,000 increase in July. The unemployment rate is projected to edge higher to 4.3%—its highest level since October 2021.”

Buckle up. It’s going to be a bumpy ride. (Or to put it another way, the VIX fear index—which measures volatility—has been elevated in recent days and was up 5.46% yesterday.)